When democracy requires more than a physics degree

Last week I gave a talk on public finance, and during the Q&A at the end, a physicist in the audience who is working on fusion research said something along the lines of “I still find our monetary system confusing”. It might have had something to do with my delivery, but I think it went deeper than that.

If a physicist who is working on one of the most complex problems of our age struggled with the concept that Parliament allocates public money by voting, what chance is there for the rest of us? Without all of us having a basic understanding of how our system of public finance works, there is no way for us to hold our politicians to account for the choices they make on our behalf.

The Treasury's black box

Here in the UK, Parliament controls the public purse. All taxation and public expenditure ultimately require statutory parliamentary authority. However, this authority only matters if those representatives know what they are authorising.

Many MPs seemingly vote on spending measures without recognising that it is their vote that initiates the monetary operations that result in new money being created. We know this must be true as we often hear them ask how we will "pay for" something, as if the government must first acquire money before it can spend. Some talk about the fear of "running out of money", when under current institutional arrangements, the UK cannot involuntarily run out of pounds. Most damagingly, they also accept Treasury assertions about fiscal constraints without the background knowledge to question them.

Whether shaped by culture, training or both, Treasury officials have a policy worldview with a narrow range of the possible and MPs, lacking the tools to push back, have no choice but to be guided by them.

Most voters reasonably think about public finance in the same way they think about their own household budgets. They think that governments must tax before spending, borrow when there is a shortfall, and repay debt from future surpluses. Politicians then reinforce those instincts with metaphors about “living within our means” or “balancing the books”.

Unfortunately, this seemingly sensible line of causation runs exactly the wrong way. It is government spending that creates money in the economy first. Taxation then withdraws it from circulation afterwards. Politicians framing this as household budgeting are getting the sequence exactly backwards. Yet it persists because it is politically useful. Spending restraint is always portrayed as sensible management of the economy rather than a deliberate choice with real costs, investment in public services is generally seen as wasteful excess, and unemployment is seen as an economic fact of life rather than a policy failure. When political debate rests on these falsehoods, voters can't tell genuine constraints from manufactured ones.

Power through obscurity

This confusion is not distributed evenly. Treasury and Bank of England officials understand the operational mechanics of reserve creation and settlement, as the legislative and academic papers spell it out very clearly, but almost no one outside those institutions reads them.

This concentration of knowledge also concentrates power. When only a handful of specialists understand the mechanics of our monetary system and policy proposals emanate exclusively from them, then whoever MPs turn to for an explanation ends up deciding what is feasible policy. Technical knowledge then becomes political leverage with no democratic oversight.

Fiscal rules plainly illustrate this. The government will announce targets for debt or deficit levels and then present them as binding constraints when in fact they are nothing of the sort. These targets are not legally binding, and because most MPs lack the background to challenge the institutional framing, these targets hold as if they were law. It’s an open question whether these rules even work on their own terms, as we discussed in Parliament recently (see Figure 3: Fiscal Rules and economic performance).

The same logic shapes spending decisions. A minister announcing funding for a program will immediately be met with journalists asking where the money will come from. This, of course, wrongly assumes that the government must first acquire money before spending. This normally ends with the minister, whether from genuine confusion or political calculation, accepting the premise and being forced to point to tax rises or spending cuts to justify his position. The actual monetary operation is not discussed at all.

Infrastructure investment is dismissed as "unaffordable" and proposals for full employment as economically dangerous without acknowledging that these judgments rest on assumptions about monetary constraints that simply don’t exist. The binding constraints are real resource and inflationary limits, not an inability to create pounds. These assumptions persist because the knowledge needed to challenge them stays locked away, out of reach of MPs and voters who are supposed to hold fiscal power.

What informed oversight requires

Democratic accountability over fiscal policy requires citizens and their representatives to understand three key things.

Sequence of operations

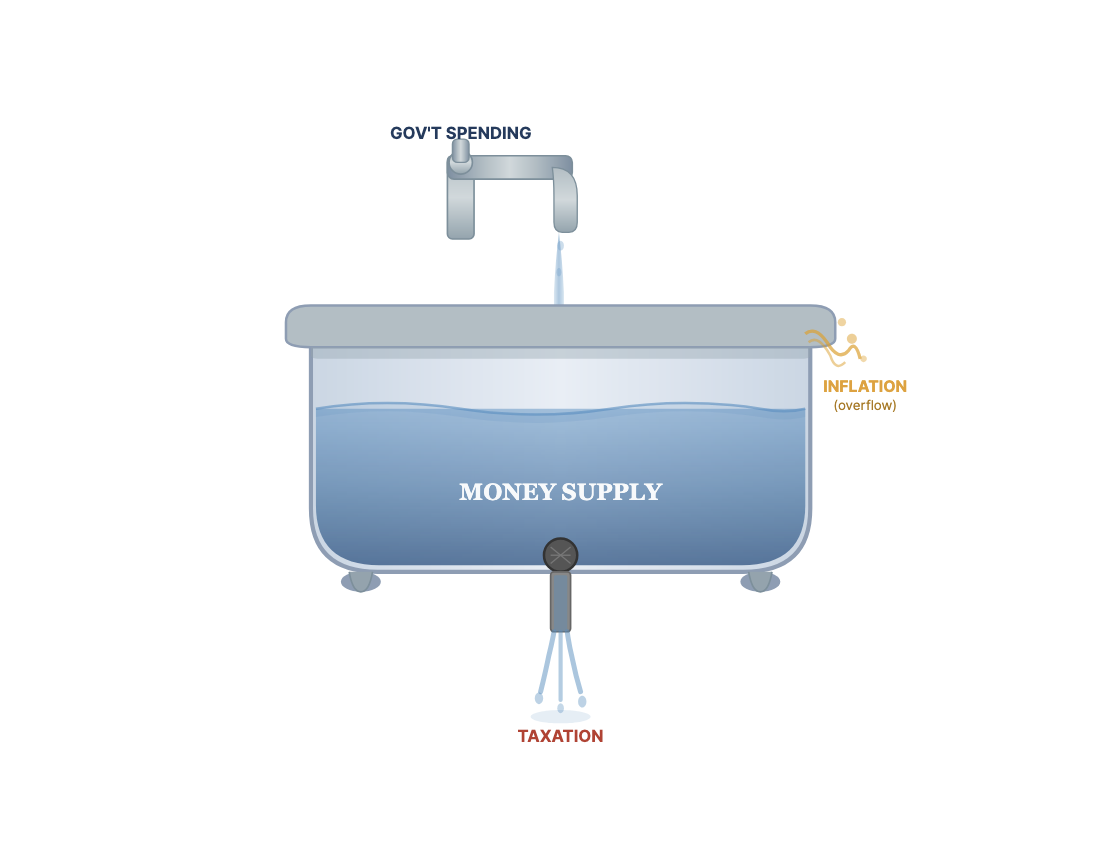

First, the sequence of operations. Net government spending adds new net financial assets to the private sector by the Treasury instructing the Bank of England to credit bank accounts in the private sector. Whether for our armed services, teachers' pay or HS2, the government instructs payments and the Bank of England complies.

Taxation then withdraws money from the system after spending. It could be no other way. Our taxes must be paid in pounds, and all pounds ultimately derive from state-issued liabilities, either directly through government spending or indirectly through the banking system operating within the state’s monetary framework.

Commercial banks also create deposits when they make loans. But those deposits exist within a system defined and backstopped by the state. All pounds, whether created through government spending or bank lending, operate within the monetary framework established by Parliament and administered by the Bank of England.

Understanding this sequence is essential. Spending introduces new net financial assets into the private sector. Taxation and bond issuance adjust the quantity and composition of those assets after the fact. The order matters. Getting it backwards leads to false debates about “where the money will come from” and obscures the real question: whether the economy has the resources to absorb the spending without generating inflation.

An imperfect but still useful mental model I use is a bathtub.

In modern UK monetary operations, government spending is not operationally dependent on prior bond sales. Deficit spending creates reserve balances in the banking system, and gilt issuance converts those reserves into interest-bearing securities. Taxes and bond sales adjust the system after spending has occurred; they do not enable it.

The real constraints

Second, the real constraints. Government spending is always limited by real resource capacity and inflationary pressures. If money creation outruns the economy’s ability to produce goods and services, then the result is inflation. This is a genuine limit that monetary sovereignty doesn’t remove. The housing market is a great example here. Over time, mortgage lending multiples increased significantly, expanding credit into a relatively inelastic housing supply, contributing to price inflation. And we wonder why we are in the mess that we are in.

Political choices

Third, the political choices embedded in fiscal decisions. When government decides not to fund a programme, this often reflects political prioritisation rather than an immediate operational inability to spend. When it tolerates certain levels of unemployment, this reflects a policy judgment about inflation risk relative to employment. These are legitimate areas for disagreement, but we should be honest and acknowledge the difference between choices and constraints.

MPs could and should challenge Treasury assertions about fiscal limits and ask whether proposed spending would generate inflation, given the available resources, rather than accepting affordability claims at face value. Voters could also then recognise that when politicians deploy household metaphors, they are likely obscuring genuine trade-offs that should be recognised and discussed.

A right, not a privilege

Everyone deserves some clarity about how government finances work and monetary literacy should not be confined to a relative handful of institutions and individuals. Understanding the legal and institutional arrangements that govern how Parliament exercises fiscal authority is no more complex than following a budget debate. In a democracy, this knowledge belongs to its citizens.

The current arrangement benefits those who seek to narrow the political debate by making certain policy options impossible when they are merely unpopular with influential actors, and it also allows government to blame external constraints for choices that reflect their political priorities.

This arrangement is perpetuated and sustained through education that teaches outdated models reflecting particular political and economic ideologies, which require mental models of “government as a household” for coherence. Most sections of the media are also complicit, often reinforcing the view that fiscal policy is technical rather than political.

The reason things don’t change is that clarity would shift power.

The physicist at my talk shouldn’t need specialist knowledge to participate in democracy. What he needs is a government that explains clearly and honestly how the system operates, and the trade-offs embedded within it. This is a democratic obligation, and we are not meeting it.

Until we do, parliamentary sovereignty is what we think we have, but Treasury dominance is actually what we get. Elections will continue to be fought over fiscal policy in language designed to obscure rather than illuminate, and democratic rituals will substitute for democratic control.

He can model plasma behaviour at 100 million degrees. He shouldn't have to guess how Parliament pays for a hospital. Neither should you.